41 duration zero coupon bond

The Macaulay Duration of a Zero-Coupon Bond in Excel The Macaulay duration can be viewed as the economic balance point of a group of cash flows. Another way to interpret the statistic is that it is the weightedaverage number of years an investor must maintain a position in the bond until the present value of the bond's cash flows equals the amount paid for the bond. Zero Coupon Bond (Definition, Formula, Examples, Calculations) These Bonds are initially sold at a price below the par value at a significant discount, and that’s why the name Pure Discount Bonds referred to above is also used for this Bonds. Since there are no intermediate cash flows associated with such Bonds, these types of bondsTypes Of BondsBonds refer to the debt instruments issued by governments or corp...

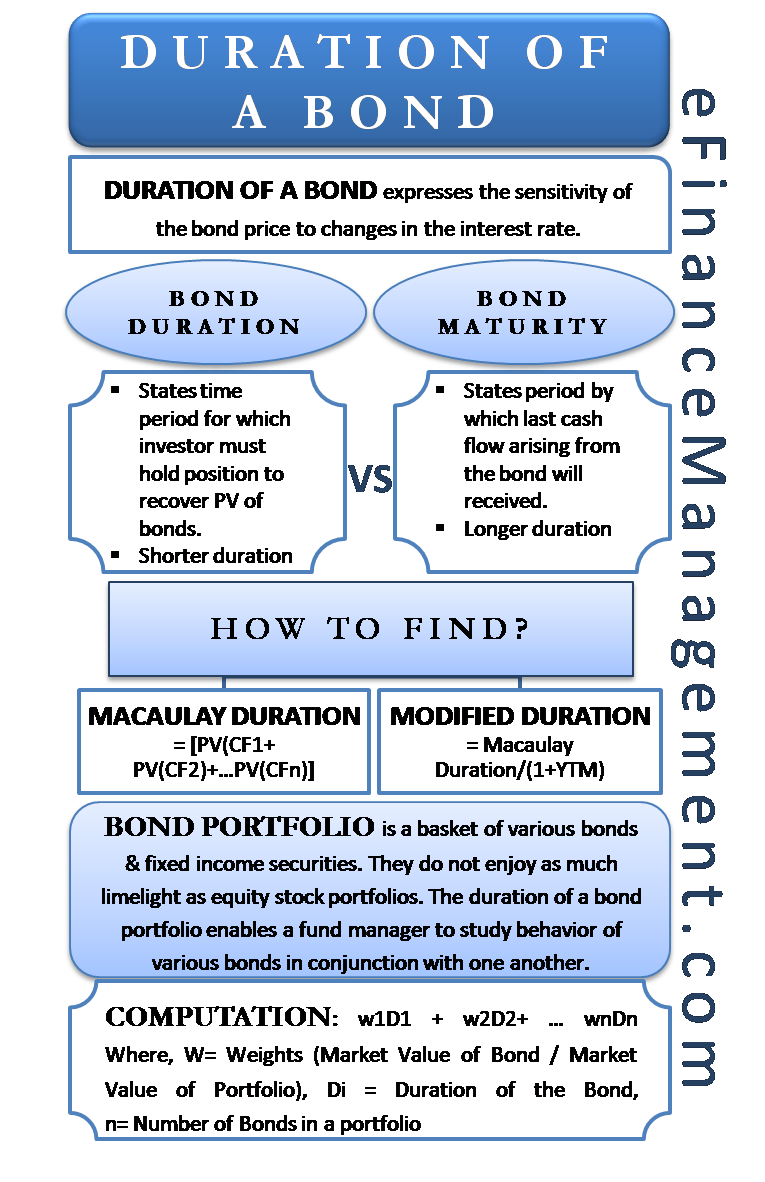

Bond Duration Calculator – Macaulay and Modified ... Bond duration is a linear estimate of a bond's price sensitivity to changes in market yield. It's the first derivative of price with respect to market yield. However – the relationship between yield and price isn't linear, it's a curve. Bond convexity is the second derivative, and a measure of the "curvedness" of the relationship.

Duration zero coupon bond

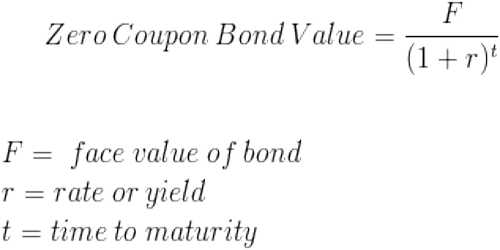

Zero-Coupon Bond - Definition, How It Works, Formula As a zero-coupon bond does not pay periodic coupons, the bond trades at a discount to its face value. To understand why, consider the time value of moneyTime Value of MoneyThe time value of money is a basic financial concept that holds that money in the present is worth more than the same sum of money to be received in the future.. The time value o... Zero-Coupon Bond - Definition, How It Works, Formula Modified Duration - Zero Coupon Bond Modified … We barely need a calculator to find the modified duration of this 3-year, zero-coupon bond. Its Macaulay duration is 3.0 years such that its modified duration is 2.941 = 3.0/ (1+0.04/2) under semi-annually compounded yield of 4.0%.

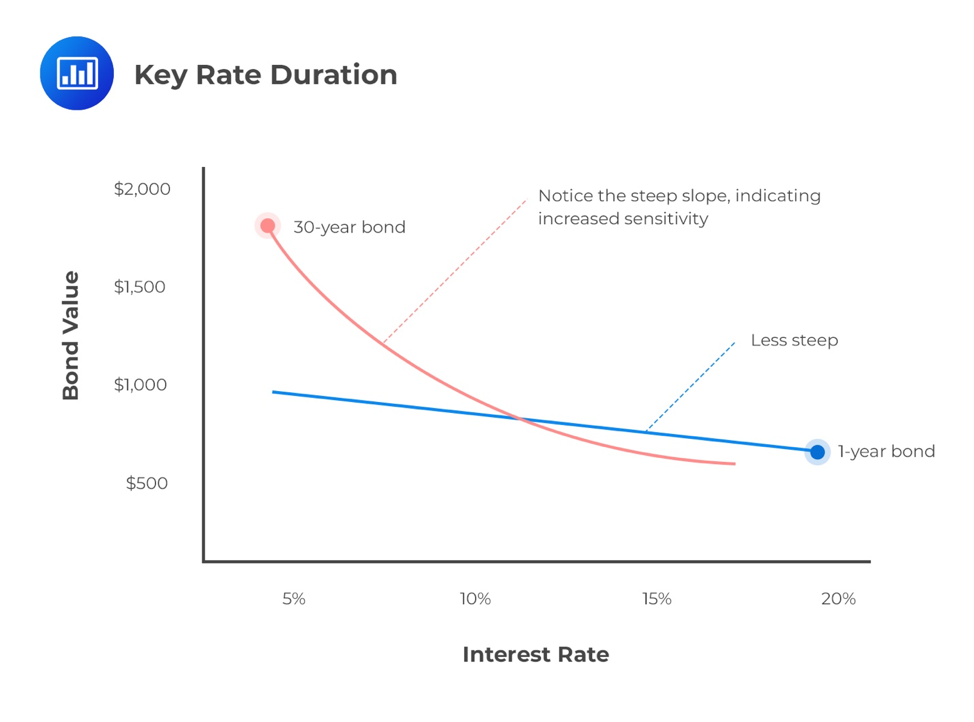

Duration zero coupon bond. What is the duration of a zero coupon bond? - Quora Zero coupon bond can be of any duration , can be from one year to 10 years. It is ordinarily from 3 to 5 years. Zero coupon bonds are issued at a discount with par value paid on redemption, sometimes with a nominal premium. Macaulay's Duration | Formula | Example 16.5.2020 · Duration of Bond A is 4.5, i.e. the maturity period (in years) of the zero-coupon bond. Duration of Bond B is calculated by first finding the present value of each of the annual coupons and maturity value. Annual coupon is $50 (i.e. … Modified duration of zero-coupond bond (FRM practice ... 28.6.2010 · A zero-coupon bond with maturity of ten (10) years has a 6% bond-equivalent yield (semi-annual compounding). What is the bond's modified duration? Understanding Duration - BlackRock rates, duration allows for the effective comparison of bonds with different maturities and coupon rates. For example, a 5-year zero coupon bond may be more sensitive to interest rate changes than a 7-year bond with a 6% coupon. By comparing the bonds’ durations, you may be able to anticipate the degree of

Zero Coupon Bond Modified Duration Formula | Bionic Turtle Our bond has a semi-annual (k = 2) yield of 4.0% so it's modified duration equals 2.641 years = 2.693 * (1+0.04/2). How can we interpret this? Duration is a ... Duration of zero coupon bond - Fixed Income - AnalystForum 10 Oct 2007 — The weight used for each cash flow is its present value divided by the total present value of the bond. In the very simple case of a zero coupon ... What is the duration of a zero coupon bond? - Quora The duration of a zero coupon bond is equal to its maturity. Duration is a weighted average of the maturities of all the income streams of a bond or a portfolio of bonds. Therefore if there are coupons, the duration will be less than the maturity, and if there are no coupons it will be equal to its maturity. 14.1K views View upvotes Quora User Macaulay Duration Zero Coupon Bond – RAEE Most bonds typically pay out a coupon every six months. A zero-coupon bond is purchased at a discount and matures at par. Basically, the bond is sold at a significant discount from its face value. The price of this zero-coupon is $554, which is the estimated maximum amount that you can pay for the bond and still meet your required rate of return.

Bond duration - Wikipedia Modified duration is a useful measure to compare interest rate sensitivity across the three. The zero-coupon bond will have the highest sensitivity, changing at ... Macaulay Duration Zero Coupon Bond – RAEE The correct answer is that with a zero-coupon bond, duration is equal to maturity as the only cash flow from the bond is the one-time payment of principal and interest upon maturity. The term originates from the time when bonds were bearer instruments, and were issued with coupons attached to them. The Macaulay Duration of a Zero-Coupon Bond in Excel Modified Duration - Zero Coupon Bond Modified … We barely need a calculator to find the modified duration of this 3-year, zero-coupon bond. Its Macaulay duration is 3.0 years such that its modified duration is 2.941 = 3.0/ (1+0.04/2) under semi-annually compounded yield of 4.0%.

Bond’s Maturity, Coupon, and Yield Level | CFA Level 1 - AnalystPrep

Zero-Coupon Bond - Definition, How It Works, Formula

:max_bytes(150000):strip_icc()/GettyImages-983195940-6d4c5099c3314718a5ba16c33205d071.jpg)

Excel中的零息债券麦考利期限-巴黎人官方网站

Zero-Coupon Bond - Definition, How It Works, Formula As a zero-coupon bond does not pay periodic coupons, the bond trades at a discount to its face value. To understand why, consider the time value of moneyTime Value of MoneyThe time value of money is a basic financial concept that holds that money in the present is worth more than the same sum of money to be received in the future.. The time value o...

PPT - Interest Rates and Bond Valuation PowerPoint Presentation, free download - ID:1723299

Advanced Bond Concepts: Duration | The Financial Engineer

Zero Coupon Bond - QS Study

Volatility of Bond Prices in the Secondary Market

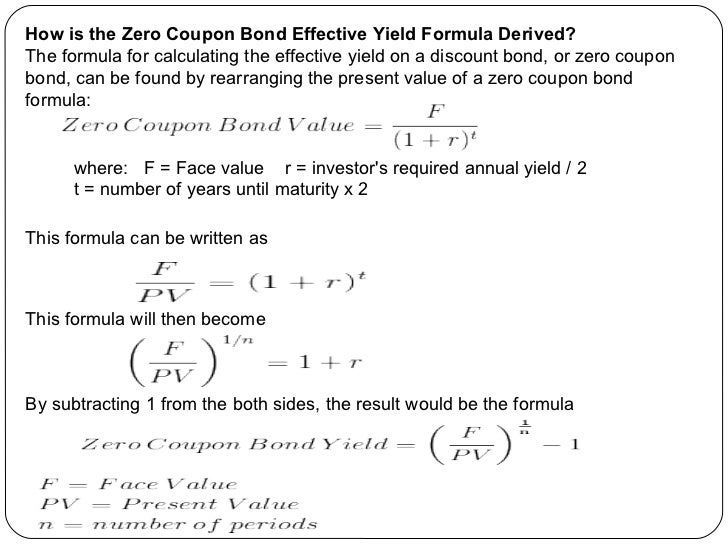

Zero Coupon Bond (Definition, Formula, Examples, Calculations)

6.3 The Zero Coupon Bond Case

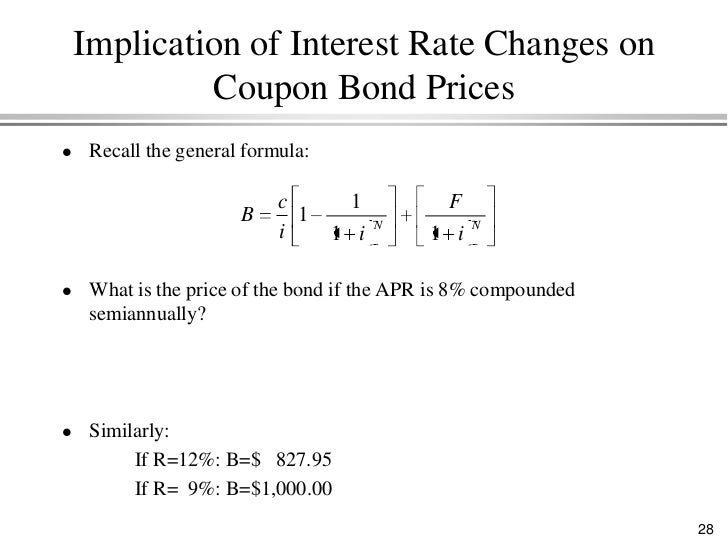

Bonds ppt

Bond valuation

:max_bytes(150000):strip_icc()/thinkstockphotos-479586547-5bfc34cf46e0fb00514690c4.jpg)

Excel中的零息债券麦考利期限-巴黎人官方网站

Essay on Bonds: Types and Valuation | Securities | Financial Management

[Solved] Bond A is zero-coupon bond paying $100 one year from now. Bond B is a zero-coupon bond ...

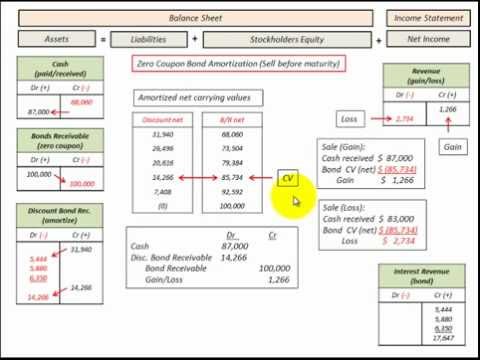

Zero Coupon Bond Sale Calculations, Accounting & Journal Entires - YouTube

Duration of a Bond | Portfolio Duration | Macaulay & Modified Duration

united states - Can zero-coupon bonds go down in price? - Personal Finance & Money Stack Exchange

Duration

Post a Comment for "41 duration zero coupon bond"